Earnings Outlook For Cactus

Author: Benzinga Insights | July 29, 2025 01:01pm

Cactus (NYSE:WHD) is preparing to release its quarterly earnings on Wednesday, 2025-07-30. Here's a brief overview of what investors should keep in mind before the announcement.

Analysts expect Cactus to report an earnings per share (EPS) of $0.70.

The announcement from Cactus is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

Past Earnings Performance

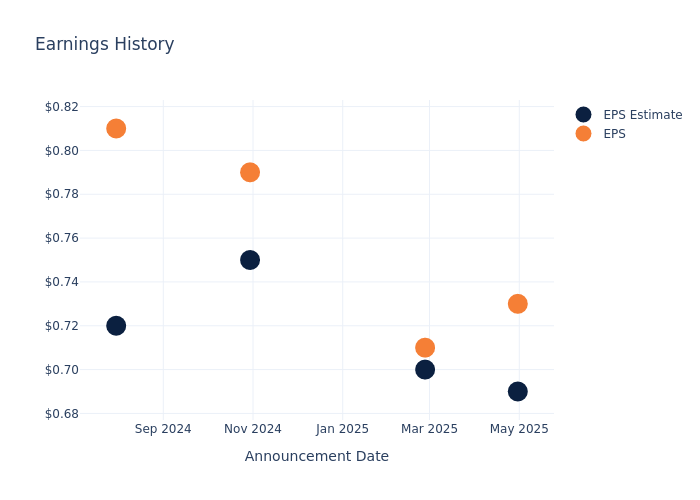

Last quarter the company beat EPS by $0.04, which was followed by a 4.64% increase in the share price the next day.

Here's a look at Cactus's past performance and the resulting price change:

| Quarter |

Q1 2025 |

Q4 2024 |

Q3 2024 |

Q2 2024 |

| EPS Estimate |

0.69 |

0.70 |

0.75 |

0.72 |

| EPS Actual |

0.73 |

0.71 |

0.79 |

0.81 |

| Price Change % |

5.0% |

-9.0% |

4.0% |

-2.0% |

Stock Performance

Shares of Cactus were trading at $47.92 as of July 28. Over the last 52-week period, shares are down 24.97%. Given that these returns are generally negative, long-term shareholders are likely unhappy going into this earnings release.

Insights Shared by Analysts on Cactus

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Cactus.

Analysts have given Cactus a total of 6 ratings, with the consensus rating being Neutral. The average one-year price target is $52.83, indicating a potential 10.25% upside.

Comparing Ratings Among Industry Peers

The analysis below examines the analyst ratings and average 1-year price targets of USA Compression Partners, Kodiak Gas Services and Tidewater, three significant industry players, providing valuable insights into their relative performance expectations and market positioning.

- Analysts currently favor an Underperform trajectory for USA Compression Partners, with an average 1-year price target of $25.0, suggesting a potential 47.83% downside.

- Analysts currently favor an Buy trajectory for Kodiak Gas Services, with an average 1-year price target of $44.0, suggesting a potential 8.18% downside.

- Analysts currently favor an Outperform trajectory for Tidewater, with an average 1-year price target of $70.0, suggesting a potential 46.08% upside.

Summary of Peers Analysis

The peer analysis summary provides a snapshot of key metrics for USA Compression Partners, Kodiak Gas Services and Tidewater, illuminating their respective standings within the industry. These metrics offer valuable insights into their market positions and comparative performance.

| Company |

Consensus |

Revenue Growth |

Gross Profit |

Return on Equity |

| Cactus |

Neutral |

2.26% |

$107.74M |

4.06% |

| USA Compression Partners |

Underperform |

6.96% |

$93.22M |

203.38% |

| Kodiak Gas Services |

Buy |

52.97% |

$130.65M |

2.22% |

| Tidewater |

Outperform |

3.82% |

$101.60M |

3.83% |

Key Takeaway:

Cactus is positioned in the middle among its peers for Consensus rating. It ranks at the bottom for Revenue Growth, indicating lower growth compared to others. In terms of Gross Profit, Cactus is at the top among its peers. However, for Return on Equity, Cactus is at the bottom, showing lower returns compared to its peers.

About Cactus

Cactus Inc is engaged in the designing, manufacturing, and sale of wellheads and pressure control equipment. Its principal products include Cactus SafeDrill wellhead systems, conventional wellheads, and production valves among others. The company also provides mission-critical field services, including service crews to assist with the installation, maintenance, and safe handling of the wellhead and pressure control equipment, as well as repair services for equipment that it sells or rents. It sells or rents its products principally for onshore unconventional oil and gas wells that are utilized during the drilling, completion (including fracturing), and production. The company has two operating segments; Pressure Control, which generates key revenue and Spoolable Technologies.

Unraveling the Financial Story of Cactus

Market Capitalization Analysis: The company's market capitalization is below the industry average, suggesting that it is relatively smaller compared to peers. This could be due to various factors, including perceived growth potential or operational scale.

Positive Revenue Trend: Examining Cactus's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 2.26% as of 31 March, 2025, showcasing a substantial increase in top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Energy sector.

Net Margin: Cactus's net margin surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 15.78% net margin, the company effectively manages costs and achieves strong profitability.

Return on Equity (ROE): Cactus's ROE stands out, surpassing industry averages. With an impressive ROE of 4.06%, the company demonstrates effective use of equity capital and strong financial performance.

Return on Assets (ROA): Cactus's ROA stands out, surpassing industry averages. With an impressive ROA of 2.52%, the company demonstrates effective utilization of assets and strong financial performance.

Debt Management: Cactus's debt-to-equity ratio is below the industry average at 0.04, reflecting a lower dependency on debt financing and a more conservative financial approach.

To track all earnings releases for Cactus visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Posted In: WHD