Exploring Healthpeak Properties's Earnings Expectations

Author: Benzinga Insights | October 22, 2025 09:03am

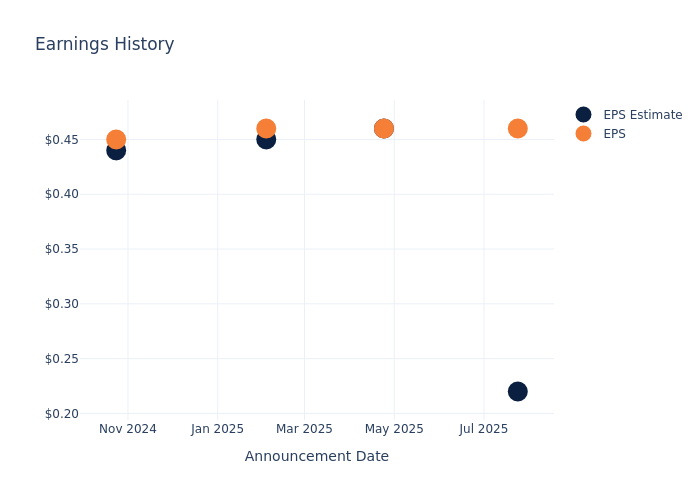

Healthpeak Properties (NYSE:DOC) is gearing up to announce its quarterly earnings on Thursday, 2025-10-23. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Healthpeak Properties will report an earnings per share (EPS) of $0.22.

The announcement from Healthpeak Properties is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

Earnings History Snapshot

The company's EPS beat by $0.24 in the last quarter, leading to a 6.73% drop in the share price on the following day.

Here's a look at Healthpeak Properties's past performance and the resulting price change:

| Quarter |

Q2 2025 |

Q1 2025 |

Q4 2024 |

Q3 2024 |

| EPS Estimate |

0.22 |

0.46 |

0.45 |

0.44 |

| EPS Actual |

0.46 |

0.46 |

0.46 |

0.45 |

| Price Change % |

-7.00 |

-5.00 |

-2.00 |

-3.00 |

Healthpeak Properties Share Price Analysis

Shares of Healthpeak Properties were trading at $18.58 as of October 21. Over the last 52-week period, shares are down 19.22%. Given that these returns are generally negative, long-term shareholders are likely upset going into this earnings release.

Analyst Views on Healthpeak Properties

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Healthpeak Properties.

With 7 analyst ratings, Healthpeak Properties has a consensus rating of Neutral. The average one-year price target is $19.57, indicating a potential 5.33% upside.

Peer Ratings Overview

This comparison focuses on the analyst ratings and average 1-year price targets of Alexandria Real Estate, Omega Healthcare Invts and CareTrust REIT, three major players in the industry, shedding light on their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for Alexandria Real Estate, with an average 1-year price target of $93.8, suggesting a potential 404.84% upside.

- Analysts currently favor an Neutral trajectory for Omega Healthcare Invts, with an average 1-year price target of $43.71, suggesting a potential 135.25% upside.

- Analysts currently favor an Outperform trajectory for CareTrust REIT, with an average 1-year price target of $37.0, suggesting a potential 99.14% upside.

Insights: Peer Analysis

The peer analysis summary offers a detailed examination of key metrics for Alexandria Real Estate, Omega Healthcare Invts and CareTrust REIT, providing valuable insights into their respective standings within the industry and their market positions and comparative performance.

| Company |

Consensus |

Revenue Growth |

Gross Profit |

Return on Equity |

| Healthpeak Properties |

Neutral |

-0.17% |

$418.17M |

0.39% |

| Alexandria Real Estate |

Neutral |

-2.37% |

$512.85M |

-0.63% |

| Omega Healthcare Invts |

Neutral |

11.78% |

$279.25M |

2.76% |

| CareTrust REIT |

Outperform |

55.27% |

$82.98M |

2.20% |

Key Takeaway:

Healthpeak Properties ranks in the middle for consensus rating among its peers. It is at the bottom for revenue growth. In terms of gross profit, it is at the top among its peers. For return on equity, it is also at the top compared to its peers.

Get to Know Healthpeak Properties Better

Healthpeak owns a diversified healthcare portfolio of approximately 700 in-place properties spread across mainly medical office and life science assets, plus a handful of senior housing, hospital, and skilled nursing/post-acute care assets, as well.

Financial Insights: Healthpeak Properties

Market Capitalization Analysis: Above industry benchmarks, the company's market capitalization emphasizes a noteworthy size, indicative of a strong market presence.

Revenue Challenges: Healthpeak Properties's revenue growth over 3 months faced difficulties. As of 30 June, 2025, the company experienced a decline of approximately -0.17%. This indicates a decrease in top-line earnings. When compared to others in the Real Estate sector, the company faces challenges, achieving a growth rate lower than the average among peers.

Net Margin: Healthpeak Properties's net margin falls below industry averages, indicating challenges in achieving strong profitability. With a net margin of 4.54%, the company may face hurdles in effective cost management.

Return on Equity (ROE): Healthpeak Properties's ROE is below industry averages, indicating potential challenges in efficiently utilizing equity capital. With an ROE of 0.39%, the company may face hurdles in achieving optimal financial returns.

Return on Assets (ROA): The company's ROA is below industry benchmarks, signaling potential difficulties in efficiently utilizing assets. With an ROA of 0.16%, the company may need to address challenges in generating satisfactory returns from its assets.

Debt Management: Healthpeak Properties's debt-to-equity ratio is below the industry average. With a ratio of 1.18, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

To track all earnings releases for Healthpeak Properties visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Posted In: DOC