Insights into Humana's Upcoming Earnings

Author: Benzinga Insights | November 04, 2025 11:01am

Humana (NYSE:HUM) is gearing up to announce its quarterly earnings on Wednesday, 2025-11-05. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Humana will report an earnings per share (EPS) of $2.86.

The announcement from Humana is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

Historical Earnings Performance

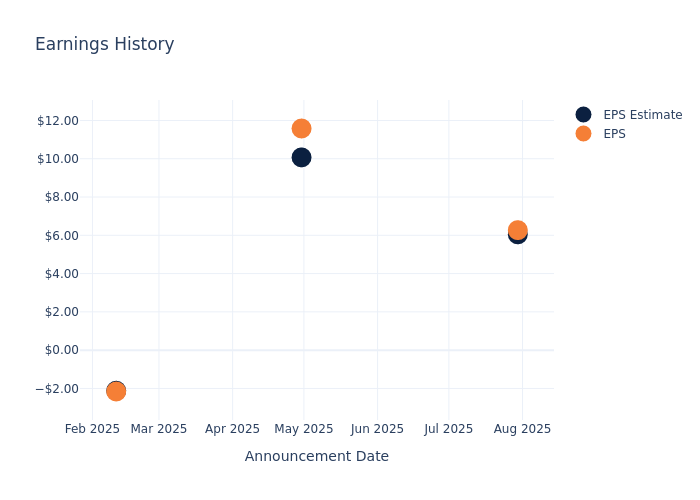

During the last quarter, the company reported an EPS beat by $0.22, leading to a 4.44% drop in the share price on the subsequent day.

Here's a look at Humana's past performance and the resulting price change:

| Quarter |

Q2 2025 |

Q1 2025 |

Q4 2024 |

Q3 2024 |

| EPS Estimate |

6.05 |

10.07 |

-2.12 |

3.40 |

| EPS Actual |

6.27 |

11.58 |

-2.16 |

4.16 |

| Price Change % |

-4.00 |

-2.00 |

1.00 |

-3.00 |

Performance of Humana Shares

Shares of Humana were trading at $279.92 as of November 03. Over the last 52-week period, shares are down 2.62%. Given that these returns are generally negative, long-term shareholders are likely unhappy going into this earnings release.

Analyst Views on Humana

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Humana.

With 11 analyst ratings, Humana has a consensus rating of Neutral. The average one-year price target is $313.45, indicating a potential 11.98% upside.

Analyzing Ratings Among Peers

The below comparison of the analyst ratings and average 1-year price targets of HealthEquity, Molina Healthcare and Alignment Healthcare, three prominent players in the industry, gives insights for their relative performance expectations and market positioning.

- Analysts currently favor an Outperform trajectory for HealthEquity, with an average 1-year price target of $121.29, suggesting a potential 56.67% downside.

- Analysts currently favor an Neutral trajectory for Molina Healthcare, with an average 1-year price target of $192.36, suggesting a potential 31.28% downside.

- Analysts currently favor an Neutral trajectory for Alignment Healthcare, with an average 1-year price target of $19.5, suggesting a potential 93.03% downside.

Insights: Peer Analysis

The peer analysis summary presents essential metrics for HealthEquity, Molina Healthcare and Alignment Healthcare, unveiling their respective standings within the industry and providing valuable insights into their market positions and comparative performance.

| Company |

Consensus |

Revenue Growth |

Gross Profit |

Return on Equity |

| Centene |

Neutral |

18.24% |

$3.25B |

-27.43% |

| HealthEquity |

Outperform |

8.64% |

$232.59M |

2.80% |

| Molina Healthcare |

Neutral |

11.00% |

$927M |

1.80% |

| Alignment Healthcare |

Neutral |

43.51% |

$125.67M |

2.46% |

Key Takeaway:

Humana ranks at the top for Revenue Growth among its peers. It is at the bottom for Gross Profit. For Return on Equity, Humana is in the middle compared to its peers.

Discovering Humana: A Closer Look

Humana is one of the largest private health insurers in the US, and the firm has built a niche specializing in government-sponsored programs, with nearly all its medical membership stemming from Medicare, Medicaid, and the military's Tricare program. Beyond medical insurance, the company provides other healthcare services, including primary-care services, at-home services, and pharmacy benefit management.

Humana's Economic Impact: An Analysis

Market Capitalization Perspectives: The company's market capitalization falls below industry averages, signaling a relatively smaller size compared to peers. This positioning may be influenced by factors such as perceived growth potential or operational scale.

Revenue Growth: Humana's remarkable performance in 3 months is evident. As of 30 June, 2025, the company achieved an impressive revenue growth rate of 9.64%. This signifies a substantial increase in the company's top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Health Care sector.

Net Margin: The company's net margin is below industry benchmarks, signaling potential difficulties in achieving strong profitability. With a net margin of 1.68%, the company may need to address challenges in effective cost control.

Return on Equity (ROE): Humana's ROE excels beyond industry benchmarks, reaching 3.03%. This signifies robust financial management and efficient use of shareholder equity capital.

Return on Assets (ROA): Humana's ROA surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 1.08% ROA, the company effectively utilizes its assets for optimal returns.

Debt Management: Humana's debt-to-equity ratio is below the industry average. With a ratio of 0.69, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

To track all earnings releases for Humana visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Posted In: HUM