A Preview Of Parker Hannifin's Earnings

Author: Benzinga Insights | November 05, 2025 09:01am

Parker Hannifin (NYSE:PH) is set to give its latest quarterly earnings report on Thursday, 2025-11-06. Here's what investors need to know before the announcement.

Analysts estimate that Parker Hannifin will report an earnings per share (EPS) of $6.64.

Anticipation surrounds Parker Hannifin's announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

Overview of Past Earnings

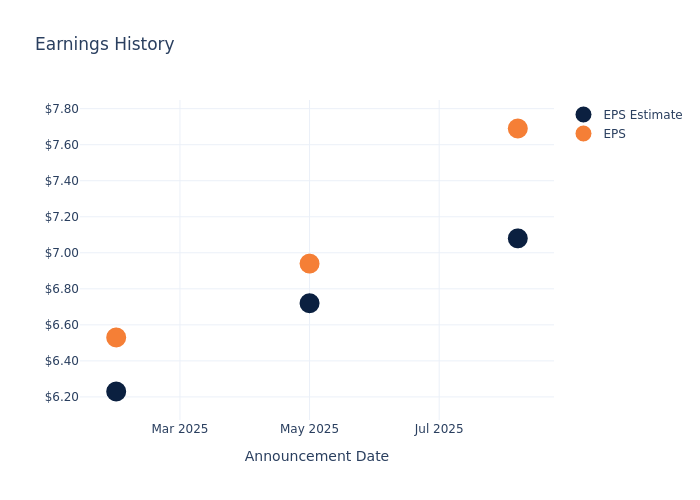

In the previous earnings release, the company beat EPS by $0.61, leading to a 0.33% increase in the share price the following trading session.

Here's a look at Parker Hannifin's past performance and the resulting price change:

| Quarter |

Q4 2025 |

Q3 2025 |

Q2 2025 |

Q1 2025 |

| EPS Estimate |

7.08 |

6.72 |

6.23 |

6.14 |

| EPS Actual |

7.69 |

6.94 |

6.53 |

6.20 |

| Price Change % |

0.00 |

1.00 |

0.00 |

0.00 |

Performance of Parker Hannifin Shares

Shares of Parker Hannifin were trading at $768.99 as of November 04. Over the last 52-week period, shares are up 11.75%. Given that these returns are generally positive, long-term shareholders should be satisfied going into this earnings release.

Analysts' Take on Parker Hannifin

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding Parker Hannifin.

Analysts have given Parker Hannifin a total of 14 ratings, with the consensus rating being Outperform. The average one-year price target is $814.86, indicating a potential 5.96% upside.

Understanding Analyst Ratings Among Peers

In this analysis, we delve into the analyst ratings and average 1-year price targets of Illinois Tool Works, Xylem and Ingersoll Rand, three key industry players, offering insights into their relative performance expectations and market positioning.

- Analysts currently favor an Underperform trajectory for Illinois Tool Works, with an average 1-year price target of $261.0, suggesting a potential 66.06% downside.

- Analysts currently favor an Buy trajectory for Xylem, with an average 1-year price target of $164.5, suggesting a potential 78.61% downside.

- Analysts currently favor an Neutral trajectory for Ingersoll Rand, with an average 1-year price target of $90.0, suggesting a potential 88.3% downside.

Peer Analysis Summary

In the peer analysis summary, key metrics for Illinois Tool Works, Xylem and Ingersoll Rand are highlighted, providing an understanding of their respective standings within the industry and offering insights into their market positions and comparative performance.

| Company |

Consensus |

Revenue Growth |

Gross Profit |

Return on Equity |

| Parker Hannifin |

Outperform |

1.08% |

$1.96B |

6.82% |

| Illinois Tool Works |

Underperform |

2.34% |

$1.81B |

25.58% |

| Xylem |

Buy |

7.79% |

$883M |

2.04% |

| Ingersoll Rand |

Neutral |

5.05% |

$855.20M |

2.42% |

Key Takeaway:

Parker Hannifin ranks at the top for Gross Profit and Return on Equity among its peers. It is in the middle for Revenue Growth.

About Parker Hannifin

Parker Hannifin started out in 1917 as Parker Appliance, selling pneumatic brakes. Through the acquisition of branded components, the firm has expanded into aerospace engines, agricultural and construction machinery, freight and passenger vehicles, and industrial automation equipment. Within these larger systems, Parker sells a wide array of small, critical pieces such as hydraulic, electromechanical, climate control, and filtration components. Many of its products are designed to work together, resulting in a high rate of cross-selling.

Understanding the Numbers: Parker Hannifin's Finances

Market Capitalization Analysis: Above industry benchmarks, the company's market capitalization emphasizes a noteworthy size, indicative of a strong market presence.

Revenue Growth: Over the 3 months period, Parker Hannifin showcased positive performance, achieving a revenue growth rate of 1.08% as of 30 June, 2025. This reflects a substantial increase in the company's top-line earnings. As compared to its peers, the revenue growth lags behind its industry peers. The company achieved a growth rate lower than the average among peers in Industrials sector.

Net Margin: Parker Hannifin's financial strength is reflected in its exceptional net margin, which exceeds industry averages. With a remarkable net margin of 17.61%, the company showcases strong profitability and effective cost management.

Return on Equity (ROE): The company's ROE is a standout performer, exceeding industry averages. With an impressive ROE of 6.82%, the company showcases effective utilization of equity capital.

Return on Assets (ROA): Parker Hannifin's financial strength is reflected in its exceptional ROA, which exceeds industry averages. With a remarkable ROA of 3.16%, the company showcases efficient use of assets and strong financial health.

Debt Management: Parker Hannifin's debt-to-equity ratio surpasses industry norms, standing at 0.68. This suggests the company carries a substantial amount of debt, posing potential financial challenges.

To track all earnings releases for Parker Hannifin visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.

Posted In: PH