How To Pick The Right Small-Cap Stocks For Your Portfolio: Fortress Vs. Zombie Small-Caps

Author: Luis Flavio Nunes | November 17, 2025 08:46am

Russell 2000 companies collectively carry over $800 billion in debt, with approximately $368 billion maturing in 2026 and another $341 billion in 2027.

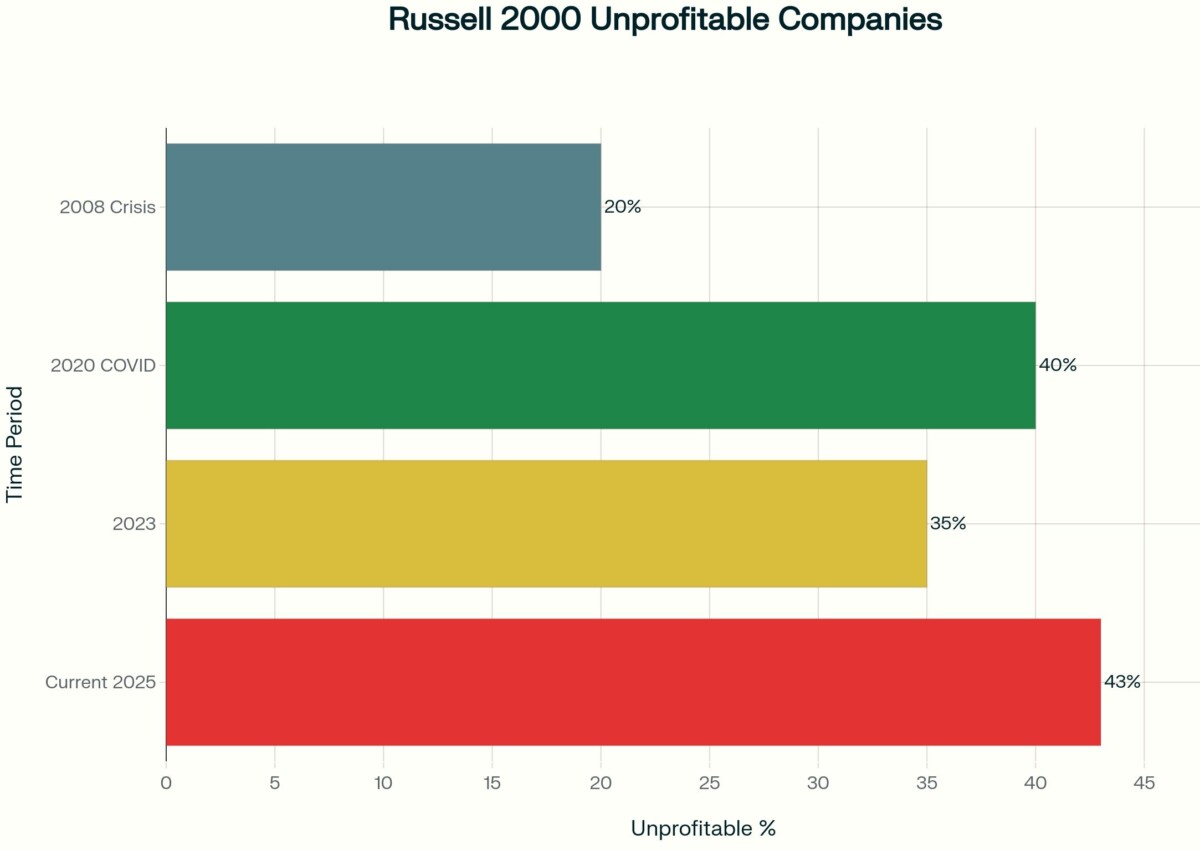

Here’s the problem, tough. 43% of small-caps are unprofitable, double the 2008 crisis level, yet they’re all being sold off together when credit concerns rise. The market can’t distinguish between fortress companies with zero debt and double-digit free cash flow margins, and zombie companies burning cash with 5x+ leverage.

For investors willing to do the work, that’s where selective stock pickers can gain an edge.

Russell 2000 High-Yield Debt Maturity Wall: $709 Billion Due in 2026–2027

The Setup: Why 2026–27 Is Different

In 2024, the market absorbed roughly $400 billion of small-cap debt and refinanced much of it without major drama. Companies that still had access to capital did the sensible thing and extended their maturities.

The 2026–27 wave looks very different:

Around 40–46% of Russell 2000 constituents are unprofitable — the highest share since COVID and roughly double the 2008 crisis level.

A larger share of borrowers are now facing refinancing at 4–5% instead of the 0.5–1% rates they locked in years ago.

Many private credit funds are already heavily committed, so they have less room to rescue every troubled borrower.

Companies that should have fixed their balance sheets in 2024 often chose to wait, or even add leverage.

For profitable, cash-generating small caps, higher rates are an annoyance. For unprofitable, overleveraged names, they can be fatal.

During the 2024 refi window, even weaker companies still had choices: sell assets, raise equity, tap private credit, and refinance on tolerable terms. As we get into 2026, those doors start to close. Lenders become pickier, equity markets less forgiving, and the gap between strong and weak balance sheets widens.

The Market's Mistake: Selling Fortresses and Zombies Together

The Russell 2000's average price-to-earnings multiple sits around 15–16x. On the surface that looks reasonable.

Underneath, the median Russell 2000 company is barely generating any free cash flow — roughly 0.06% margin versus 7.78% for the Russell 1000. Investors are paying a similar multiple for a much weaker cash profile.

At the same time:

Many fortresses small caps with solid balance sheets trade around 14–16x earnings.

Comparable large-cap quality often trades closer to 20–25x.

That 30–40% gap has little to do with fundamentals and a lot to do with labels. Investors are paying up for big-cap quality and discounting small-cap quality, even when the underlying metrics look similar or better on the small-cap side.

Whenever a zombie small cap misses earnings or a credit headline hits the tape, index funds and ETFs sell the whole bucket. Forced selling doesn't matter whether a company has $700 million of net cash or is on the verge of a covenant breach.

That's the kind of blunt selling that leaves mispriced opportunities for investors willing to read balance sheets and cash flow statements instead of just tickers.

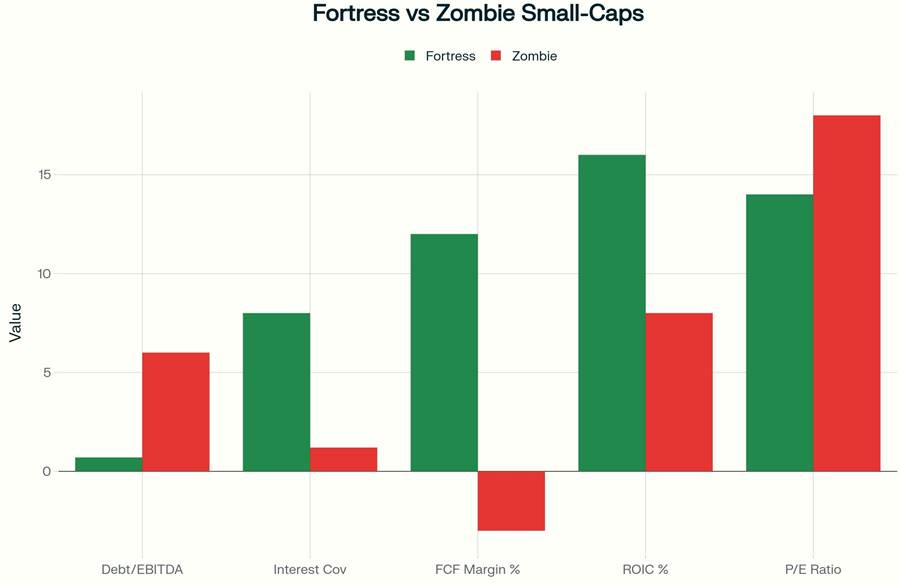

Fortress vs. Zombie: What You're Actually Buying

You don't need specialized credit training to see the difference. You just need to know what to look for.

Fortress small caps tend to show:

Debt-to-EBITDA below 1.0x (or no debt at all)

Free cash flow margins around 10% or higher, preferably mid-teens

Interest coverage comfortably above 5x

No major debt maturities in 2026–27

A history of steady dividends or buybacks funded from real cash generation

Recurring revenue or clear pricing power

Return on invested capital north of 15%

These are the businesses that don't need to beg lenders for help during a credit squeeze. They can keep investing, keep paying shareholders, and pick off competitors that run into trouble.

Zombie small caps tend to look like this instead:

Debt-to-EBITDA above 5.0x

Negative free cash flow for several years in a row

Interest coverage under 1.5x

Large chunks of debt maturing in 2026–27, often equal to 30% or more of market cap

No dividend track record, or cuts in recent years

Exposure to industries under structural pressure

These are the names that will struggle to refinance on acceptable terms. When they finally do a deal, it often comes with double‑digit coupons, heavy dilution, or both.

Fortress vs. Zombie Small-Caps: Financial Metrics Comparison

Metric

Fortress Target

Zombie Red Flag

Debt/EBITDA

Under 1.0x

Above 4.0x

Interest coverage

Above 5x

Below 3x

Free cash flow margin

Above 10%

Negative

ROIC

Above 15%

Below 10%

2026–27 maturities

Small vs. market cap

30%+ of market cap

This table won't catch every nuance, but it's a useful first screen.

Comfort Systems USA: A Fortress in Plain Sight

Comfort Systems USA (NYSE:FIX) is one example of a small-cap profile that fits the fortress description using current numbers:

Net cash position around $725 million as of Q3 2025, so no net debt to refinance

Free cash flow margin of roughly 21.2% in Q3 2025, up from the mid‑teens a year earlier

Trailing 12‑month EBITDA of about $1.25 billion, up more than 70% year‑over‑year

Backlog of roughly $9.4 billion, giving solid revenue visibility into 2027

Essential HVAC and plumbing services that customers can't easily delay

A company with this profile does not depend on friendly credit markets. It can fund growth internally, keep paying shareholders, and look for smart acquisitions while weaker competitors scramble to roll their debt.

Yet businesses like this are often priced as if they're just as fragile as the weakest names in the index. They move with the Russell 2000 on bad days even though their balance sheets look completely different.

(Details here are for illustration, not a recommendation to buy or sell any security.)

How to Find Fortress Small Caps

You can build a short list of candidates using five simple metrics in any stock screener:

Free cash flow margin above 10%, confirmed for at least three years

Return on invested capital above 15%

Valuation in the low‑to‑mid‑teens on earnings, cheaper than similar large‑cap peers

To tighten the list further, add a few extra filters:

No significant debt due in 2026–27 when you read the latest 10‑K

At least five years of stable or rising dividends

Insider share buying at recent prices

Analysts slowly revising estimates higher

Run these checks and you'll quickly reduce the Russell 2000 from a broad index to a manageable watchlist of higher‑quality names.

How to Flag Zombie Candidates

It can also help to keep a separate list of names you don't want to own.

If a Russell 2000 company checks most of these boxes, treat it as a zombie candidate:

Debt-to-EBITDA above 5.0x

Negative free cash flow two years in a row or more

Interest coverage below 1.5x

Debt maturing in 2026–27 equal to 30% or more of market cap

A business model facing obvious long‑term headwinds

When these companies go to refinance, you often see terms that tell you all you need to know: high‑teens coupons, bondholder concessions, heavy equity issuance. That's not the kind of setup you want to own into a credit shock.

Number of Russell 2000 Unprofitable Companies: 2008 Crisis (20%) vs. 2020 COVID (40%) vs. 2023 (35%) vs. Current 2025 (43%)

What Could Trigger the Break Between Fortresses and Zombies

The market will not draw a clean line between strong and weak balance sheets until there's a visible stress event. Some things to watch starting in 2026:

A first wave of Russell 2000 bankruptcies or distressed exchanges

High‑yield credit spreads widening from the mid‑300s to 600 basis points or more

Rating agencies cutting a cluster of overleveraged small‑cap names

Borrowers being forced into refinancing at double‑digit coupons

Analysts shifting tone from “soft landing” to open concern about credit quality

When one of these moments hits, the first reaction is usually indiscriminate selling. Index products sell small caps broadly. Fortress names drop 10–15% along with the weaker crowd.

That phase rarely lasts. Once investors see which companies have strong cash generation and little to refinance, money tends to rotate back toward those stocks and away from the true problem names.

Questions to Ask Before You Buy

Before putting capital into any small‑cap candidate tied to this theme, walk through a short checklist:

Can you point to three years of positive free cash flow in the filings?

Is there little or no debt maturing before 2028?

Does EBIT cover interest by at least five times?

Have insiders been buying shares near current prices?

Does management address upcoming maturities clearly on calls and in presentations?

Would you still be comfortable owning the stock if it dropped 20% on nothing but sector headlines?

If several of these answers are “no,” it may be better to keep the name on your watchlist and wait.

How to Build a Position

This is not a three‑week trade. The debt wall plays out over several years, and so does the market's response.

A practical way to approach it:

Think in a three‑to‑five‑year window. The early gains are likely to come as investors recognize which companies don't face refinancing risk. The later gains come from business growth and higher margins as weaker competitors exit.

Keep single‑stock exposure modest. Two to three percent of your portfolio per fortress name, and 10–18% for the entire basket, is enough to matter without taking on outsized risk.

Spread your entry over time. Start with half of your intended position, then add the rest over three to six months as you see more earnings reports and credit data.

Prefer weakness to strength when adding. Build positions when the Russell 2000 is under pressure or when quality names are down on sector fear rather than bad company news.

Review holdings quarterly, not daily. After each earnings season, check cash flow, debt levels, backlog, and dividend policy. If the numbers still fit the fortress profile, short‑term volatility becomes easier to live with.

When the Market Is Likely to Catch On

The timing won't be perfect, but a rough roadmap looks like this:

Q1–Q2 2026: First signs of stress. Some weak borrowers struggle to refinance, and a few small‑cap defaults hit the tape. High‑quality balance sheets start to matter more in analyst notes.

Q2–Q3 2026: The separation becomes clearer. Fortress small caps show steadier performance than the index, and more capital starts to flow into dedicated baskets of higher‑quality small caps.

Q3 2026 and beyond: The story becomes mainstream. Media coverage focuses on “winners and losers” from the debt wall. By then, much of the easy rerating in fortress names may already have happened.

That's why doing the work in late 2025 and early 2026 matters. You don't need to pick the exact day credit spreads widen. You just need to already own solid balance sheets when the market finally starts paying attention to them.

The Bottom Line: Don't Buy "Small Caps" – Buy Fortresses

Russell 2000 companies face a real refinancing test in 2026–27: roughly $368 billion in 2026 maturities and $341 billion in 2027. A large slice of the index is not ready for that.

At the same time, there is a group of fortress‑style small caps with low debt, strong free cash flow, and little to refinance in that window. They're being priced as if they're no safer than the weakest borrowers.

If you can consistently distinguish between zombies and fortresses, the coming small-cap shakeout doesn't have to be something you fear. It can be the moment you waited to accumulate durable small-cap compounders while most of the market is still dumping everything with a small-cap label.

This article is for informational purposes only and does not constitute investment advice. Always do your own research and consider your risk tolerance before investing. The author has no position in any companies mentioned at the time of writing.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.