Where Will Europe Source Its Precious Metals? The Continent's Gold, Silver, and Copper Production Outlook

Author: European Capital Insights | November 17, 2025 08:58am

Europe faces a critical question: where will it secure precious metals as global supply chains fracture amid rising geopolitical tensions? The continent's mining sector, long overshadowed by major suppliers in Canada and Australia, is now under pressure to reduce its reliance on imports.

Currently, the European Union (EU) imports around 50% of its copper concentrate – a risky position given the polarized world and accelerated nearshoring by China and the US. In response, the EU has designated 47 strategic projects to secure access to critical minerals and reduce import risks.

The EU's domestic copper reserves are modest. At around 41 million metric tons, that's a minor part of about 1.2 billion metric tons in global reserves concentrated primarily in Chile, Australia, Peru, and the Democratic Republic of Congo.

The EU, as well as the US, is scrambling to reduce its dependency on China and other suppliers of precious metals and other critical minerals for national security. Beijing has tightened export controls on rare earths and critical minerals this year, sparking concerns about global supply chains.

"Dismantling Beijing's critical raw material weapon requires a sweeping emergency policy package to wean Europe off Chinese supply as soon as possible," the EU Institute for Security Studies wrote. Europe must build its "own geo-economic tools as a deterrent and combine this with a bold reindustrialisation agenda to salvage its prosperity."

EU Has Options to De-Risk from China

The EU has supply options to derisk its supply chains from China, particularly in precious metals. Currently, the leading European producers leverage advanced operations across Scandinavia, Poland, and Russia. Agnico Eagle's (NYSE:AEM) Kittila mine in Finland represents one of the EU's best gold operations, generating 218,860 ounces in 2024.

The Finnish operation benefits from automation technologies and renewable energy integration, positioning it among the continent's lowest-cost producers with all-in sustaining costs below $1,300 per ounce.

Poland's KGHM Polska Miedź is the largest European copper producer, with an annual output of nearly 700,000 metric tons. The state-owned enterprise operates major underground complexes, including Polkowice-Sieroszowice and Rudna, where copper extraction produces significant silver as a byproduct. These operations produced 1,533 metric tons of silver in 2022, establishing the country as Europe's leading silver producer.

Map of operating mines in Europe, Source: GeoERA.eu

Swedish mining leader Boliden (OTCPK: BDNNY) operates strategically essential mines, including Aitik and Garpenberg. The latter is one of the world's most efficient underground zinc mines with significant silver output.

In 2024, it produced 8.23 million ounces, ranking #17 on the global silver production list. Boliden has focused on sustainable practices, including electronic waste recycling and carbon capture. Its revenues reached around €6.5 billion in 2024.

Russia's Norilsk Nickel maintains substantial copper production with the Norilsk complex producing around 350,000 metric tons per year, alongside nickel and palladium. First-quarter 2025 output reached 109,355 metric tons, demonstrating operational stability despite challenging Arctic conditions.

Unless the current political situation is resolved, Russian commodities, primarily produced at the Kola Peninsula near Murmansk, will not reach the EU supply chains.

Notable Exploration Activities Within The EU

Among the ongoing greenfield discoveries and brownfield expansions, Canada's Group Eleven Resources (OTCQB:GRLVF) has emerged as a promising player in Ireland's prolific zinc district.

The firm holds around 549 square kilometers of prospecting licenses across three main properties. The exploration has made notable discoveries at the PG West project, intercepting high-grade mineralization, including 39.7 meters grading 9.5% zinc and lead, plus 131 grams per ton silver. Deeper copper-silver zones return grades up to 3.72% copper and 838 g/t silver.

Group Eleven's strategic position, adjacent to Glencore's (OTCPK: GLNCY) Pallas Green deposit, reduces exploration risk, while the company benefits from Ireland's infrastructure-rich environment and favorable mining jurisdiction.

Neighbouring Glencore holds a 17.1% stake through its Glencore Canada subsidiary, providing strategic validation but also sparking rumors of potential M&A activity.

Finland's exploration sector shows promise with Arctic Minerals' Hennes Bay project. The project has an inferred resource of 55.39 million tons grading 1.0% copper equivalent, containing 447,000 tons of copper and 37 million ounces of silver.

In Greece, Eldorado Gold is advancing projects including Olympias and Skouries, while planning low-impact mining practices amid regulatory scrutiny. The latter is set to start production in 2026, targeting 140,000 ounces of gold and around 30,000 metric tons of copper per year.

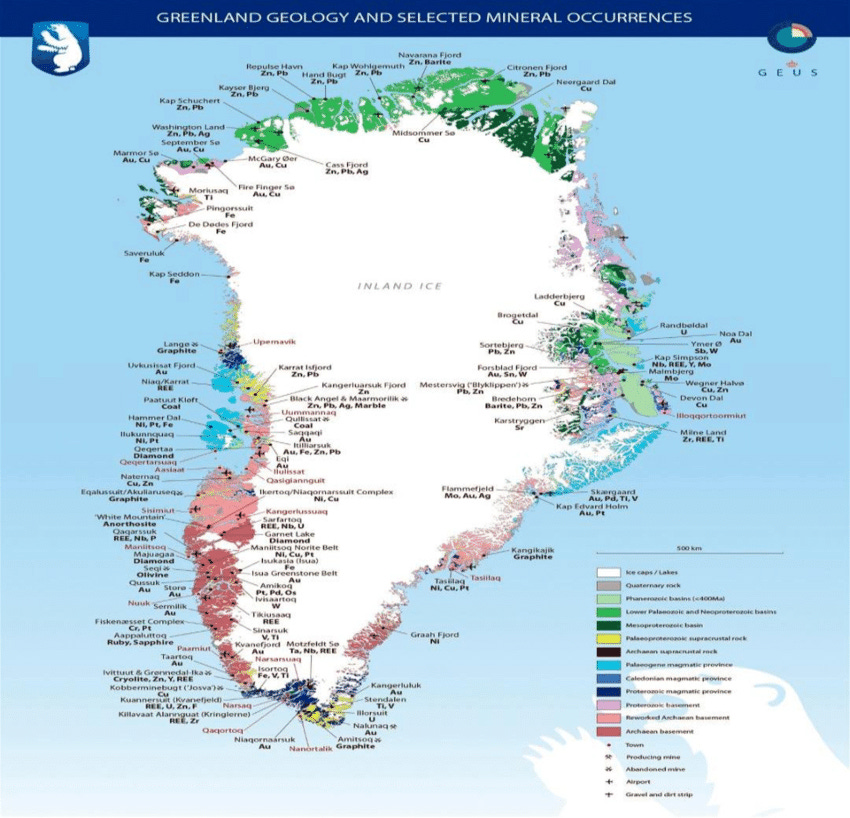

Greenland's Gold Mining Has Potential

Greenland, as a Danish territory, offers substantial untapped potential despite infrastructural challenges.

The island's strategic position and vast commodity wealth have sparked discussions earlier this year, following US President Donald Trump's repeated suggestions to purchase the territory.

Greenland's mineral deposits, Source: ResearchGate

While rare earth elements kept Greenland in the headlines, its gold mining potential remains notable. Last month, Amaroq Minerals reported discoveries with grades up to 38.7 grams per ton across multiple sites in the Nanortalik Gold Belt.

The company's Nalunaq gold mine resumed production in late 2024 following approvals for environmental and social impacts, with inferred resources supporting one of the world's highest-grade gold operations. Greenland's mineral potential extends to copper, with Amaroq identifying gold-copper systems at Isortup Qoorua, including assays of 1.98% copper.

Countries Eyeing EU Membership Could Help

Countries gravitating toward EU economic integration present additional opportunities for mineral development.

In Serbia, Chinese-controlled Zijin Mining is executing a massive expansion of the Bor Copper Complex and the Cukaru Peki mine, targeting 290,000 metric tons of copper in 2025, with long-term goals of reaching 450,000 tons annually. The company's $3.5 billion investment plan includes drilling to depths of up to 2 kilometers and expanding throughput to 15,000 tons per day, positioning Serbia as Europe's second-largest copper producer.

Serbia's political uncertainty continues to pose a risk to large-scale investment. Rio Tinto (NYSE:RIO) has just mothballed the $3 billion Jadar lithium project, citing the project's lack of permitting progress.

Bosnia and Herzegovina's mining sector centers on Adriatic Metals' (OTC:ADTLF) Vares project, which entered commercial production in July 2025 after declaring sustained operational stability. The polymetallic operation is currently ramping to nameplate capacity of 800,000 tons per annum, extracting copper, silver, lead, zinc, and gold with investments exceeding €200 million.

Europe vs. Traditional Mining Jurisdictions

European mining projects face substantially longer development timelines than those in traditional mining regions, creating competitive disadvantages that discourage investment. In Canada or Australia, permitting can be completed within 2 years under optimal conditions.

European processes face significant regional variability. The European mining bureaucracy has historically focused on environmental protection and stakeholder consultation. The EU's evolving regulatory framework encompasses environmental impact assessments, waste management obligations, and community consultations, often extending project timelines beyond those in competing jurisdictions.

Northern European jurisdictions, including Scandinavia, achieve relatively efficient approvals, with 49% of mining executives reporting permits granted within six months, outpacing even these traditional mining leaders. Canadian processes, despite averaging two years, can extend to 15 years for complex projects involving Indigenous consultations and environmental reviews, yet maintain greater transparency than their European counterpart.

"The EU has equipped itself with a wide variety of legislative and regulatory tools to try to ensure that China cannot gain too much influence through its economic leverage," Ian Bond at the Centre for European Reform wrote on October 14. "The strategy remains a patchwork of tools largely applied at the national rather than the EU level, which results in varying degrees of effectiveness in its application."

Disclaimer:

Any opinions expressed in this article are not to be considered investment advice and are solely those of the authors. European Capital Insights is not responsible for any financial decisions made based on the contents of this article. Readers may use this article for information and educational purposes only.

Benzinga Disclaimer: This article is from an unpaid external contributor. It does not represent Benzinga’s reporting and has not been edited for content or accuracy.